Benchmarking Multi Product Penetration in Software

Datadog trumps all in Software, Databricks on track to have the fastest new product launch in software history, Apps vs Infrastructure debate

Updating some thoughts after positive feedback from the original post on benchmarking product penetration in Software. I have updated the dataset to now include Databricks’ latest numbers, as well as product penetration data from CRM, CRWD, DDOG, WDAY, ZM. The total dataset now encompasses 17 public software companies, split pretty evenly between Application and Infrastructure companies.

*Chart excludes DDOG/WDAY to better show scaling. Chart with full dataset below*

The biggest takeaways from looking at this new dataset are:

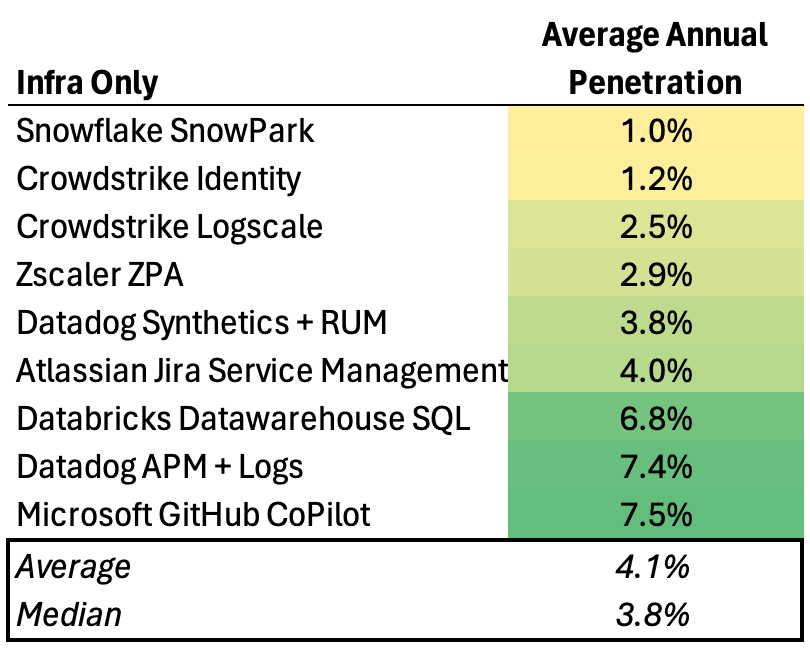

Average annual new product penetration of ARR across the 17 vendors is ~3% per year

Salesforce was able to take Service Cloud to 25% of revenue 6 years after the launch in 2009. This makes CRM the most successful/fastest penetration among Application Software companies (~4.5% penetration of ARR per year). Service Cloud was a natural adjacency for Salesforce to expand from Sales Cloud.

Workday launched Financial Management/ERP in 2008 & it took ~8 years for the company to get to ~8% of revenue. WDAY’s expansion into ERP was very hard as the buying center for HCM was completely different than the one for ERP. The acquisitions of Adaptive/ScoutRFP added ~7pts to ERP penetration of ARR in 2018/2020 respectively. Today ERP penetration of ARR has stalled out at ~25% (similar to CRM’s penetration ceiling of ServiceCloud), an average annual penetration of ~2% per year.

Zoom was able to leverage its massive Video installed base by getting Zoom Phone to ~11% of Revenue in ~4.5 years. ZM chose to massively discount this product vs the market, with an implied $6 per seat per month vs the industry’s $15-$20 per seat per month pricing.

Datadog clearly stands out and their disclosures speaks to their ability to expand into other areas of observability. The company was able to get APM + Logs (although 2 separate products) to ~45% of ARR in ~5 years post launch. Given the disclosures from the company are including 2 products, it’s fair to assume they are similar/equal in size, meaning DDOG has gotten each product to ~22% of revs in 5 years (~4-5% per year).

Databricks new disclosures show that their Datawarehouse product is approaching ~17% of ARR, only 2.5 years post launch of the product. Based on all public data, this seems to be the fastest new product launch in terms of ARR penetration in the Software landscape currently

Github Copilot ARR has 3xed in 2 years to $300m & ~15% of Github ARR penetration (as of June 24 MSFT earnings). This trajectory rivals Databricks performance

Infra Software companies new product penetration of ARR is close to 2x that of Apps companies. Infra companies tend to be more PLG and bottoms up driven which could explain the difference, in addition to the virality that products tend to have with developers, vs front office app end users

Full Raw Data Table:

**Sources:

Atlassian: Blog Post GA, 2024 Investor Day

Crowdstrike: Various Earnings Calls

Datadog: Various Earnings Calls. APM launched in Feb 2017, Logs Launched in Mar 2018 (for sake of simplicity took midpoint of those given metric disclosed). Synthetics launched June 2020, RUM launched Dec 2019.

Databricks: Bloomberg article, TechCrunch Article, Blog Post GA

Freshworks: S-1 Timeline, 2023 Investor Day

Hubspot: 2020-2024 Analyst Days

Monday.com: 2023 Investor Day, Sales CRM Blog Launch

Microsoft: The Information, Earnings Calls

Salesforce: Press Releases. Service Cloud was GA in 2009.

Snowflake: 4Q24 Earnings Call, Blog Post GA

Workday: Earnings Calls, Investor Days. Adaptive acquisition added ~6pts of penetration in FY19, ScoutRFP Acquisition added ~1pt of penetration in FY21.

Zscaler: Various Earnings Calls

Zoom: Earnings Calls, using ~$6 per seat per month assumption, implied taking ZM disclosures on seats + revenue

Such a timely post! Was asked this exact question at work today

This data is amazing, thanks for pulling this together. Super powerful to see the data test some of the conventional wisdom re: multi-product playbooks in app v infra saas