Understanding Multi Product Adoption in Software

Why Snowflake is in trouble and why Monday.com could be the next Hubspot

Why Multi Product Adoption is Important

Both Salesforce (CRM) and ServiceNow (NOW), among the largest public Software companies, have shown us how critical it is for product expansion to drive topline growth but also expand customer LTV, improve sales efficiency, and drive operating leverage.

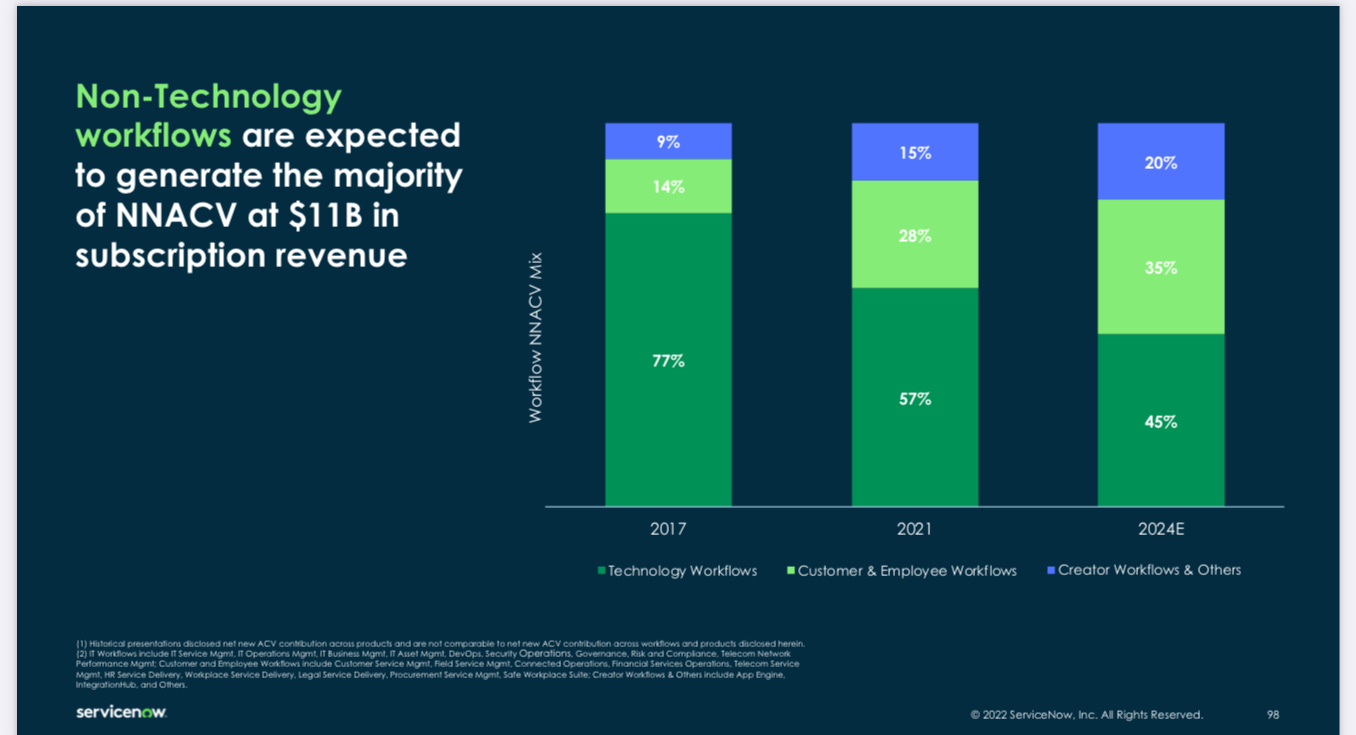

Starting with topline, lets look at ServiceNow (NOW), a company that that had some debating the size of TAM or durability of growth (see short report from 2012 here), has expanded into a variety of other products outside of ITSM including HR and ERP workflows. This has allowed NOW to maintain impressive level of growth, most recently growing 25% on a $10bn annual subscription revenue run rate.

Source: ServiceNow 2022 Investor Day

Adding new products are critical to expanding margins as they often can come come at very high gross margins (if can leverage existing infra/COGS), in addition to improving sales efficiency as sales reps can now sell more into an existing customer that they’ve already landed and spent money on, ultimately increasing their LTV.

Source: Salesforce.com 2015 Investor Day

Multi Product Adoption at Maturity

What is a “good” rate of penetration for new products over time? A few rules of thumb we can use based on publicly available data:

Salesforce.com is likely the oldest example we have in terms of public available data. ServiceCloud was introduced in 2009 and by 2017 it was ~30% of Subscription Revenue on a +$7bn base.

ServiceNow has seen Non IT Workflows go from ~25% of NNACV in 2017 to targeting ~55% of NNACV in 2024

ServiceNow’s Pro SKU has seen 45% penetration inside the installed base since launching in Sept of 2018

MSFT E3 SKU’s have on average seen 5% annual penetration

Successes of Driving New Product Adoption

Success Story: HubSpot is the among the best examples of the “next gen” SaaS vendors in terms of creating a multi product machine. HubSpot has been successful in leveraging their position in the Marketing side and extending to natural adjacencies like CRM, and then into Customer Service. HubSpot had a very good Marketing product for SMBs, and their unit economics allowed them reinvest into other areas of the stack + hire more sales capacity. The key here is that in the case of HubSpot, they were able to replace point vendors with the value proposition of having a single common data model, in which customers can use the same data/database for different workflows/functions. As of Q223, HUBS has 27% of ARR coming from Sales Hub, 6% of ARR coming from Service Hub, and ~7% of ARR coming from both CMS and Operations Hub.

Source: HubSpot 2022 Investor Day

Where Multi Production Adoption Can Go Wrong

Freshworks (FRSH) on the other hand, has had a very hard time of scaling into a successfully multi product company. The company started off in the ticketing side of Customer Service with their Freshdesk product (similar to Zendesk) and then expanded into ITSM (FreshService). Interesting enough, FRSH did very well with its ITSM product, which most recently was reported to be growing 40%+ on a $260m ARR base.

The biggest problem however, is that the rest of the portfolio has been slowing down a lot, primarily the core Freshdesk product (Zendesk competitor). There are a few reason for this including the buyers for each of these products being different (lack of cohesive GTM strategy) and lack of production integration/workflow. One could argue 1)FRSH’s core product was not differentiated enough or not in a big enough market 2) FRSH expanded to quickly and had to port more $’s into the faster growing product FreshService, leaving the existing product Freshdesk open for carnage.

FreshService (the “non core product”) is now 40%+ of ARR, and the rest of the business is slowing down noticeably (growing LDD%). So while they have 2 products with +$250m in ARR each and high penetration of another product, their strategy didn’t prove to be as as successful as HubSpot.

Source: Freshworks

Benchmarking Public Software Companies in New Product Adoption

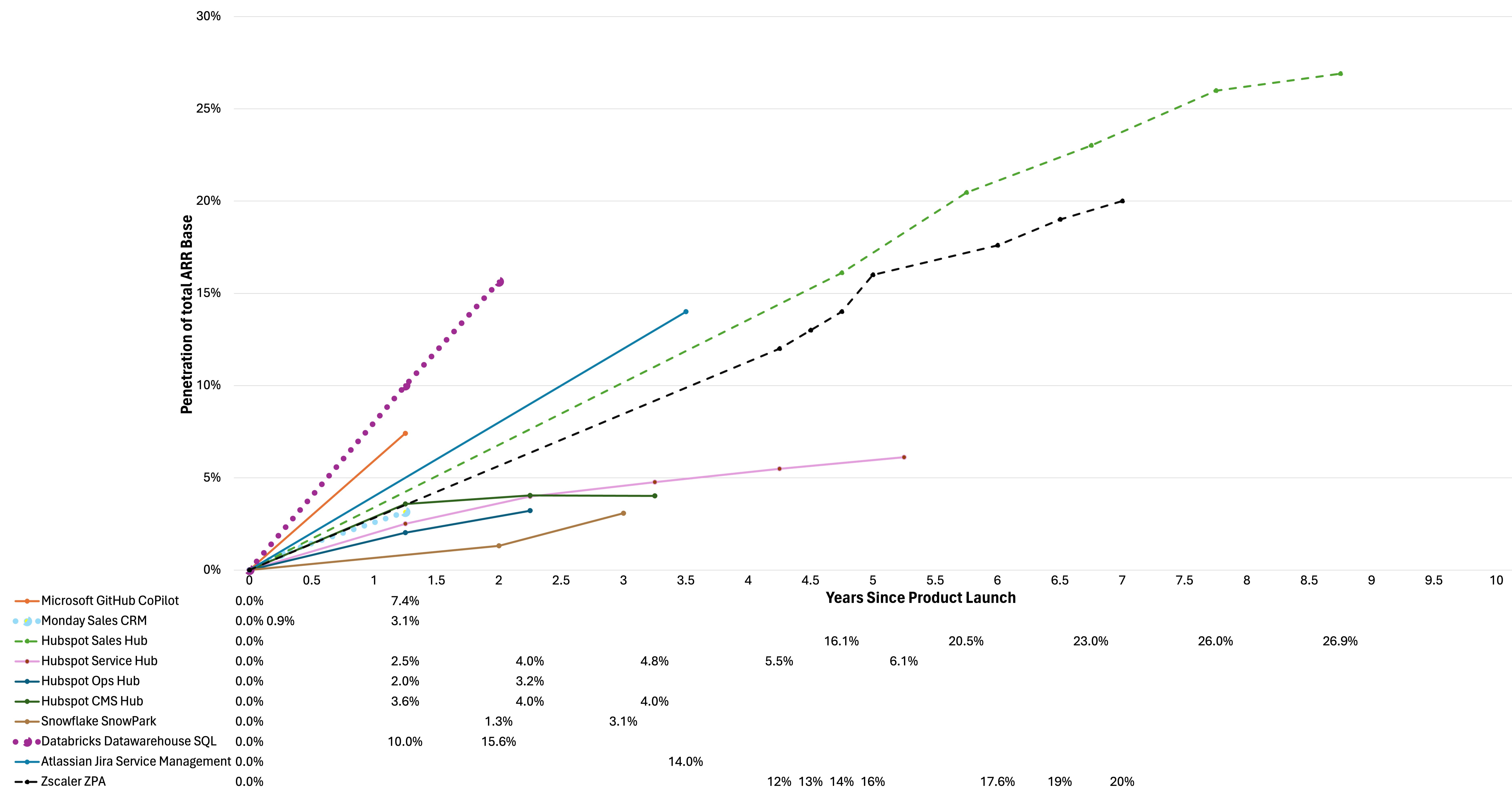

Ok if you’ve made it this far congrats, this is what you’ve been waiting for. Despite the lack of disclosure that many public software companies give, there are enough bread crumbs for public equity investors to look compare New Product adoption inside scaled software businesses. Mapped out below is the product adoption curve of many prominent software businesses today. The Y Axis shows the respective new product penetration of total company ARR and the X axis shows the period of time since product launch (extended out to 10 years).

**Sources: Below

Main Conclusions:

HUBS clearly is the standard among the newer software companies (Ex NOW/CRM that are at maturity). Sales Hub penetration went from 16% of total ARR after 4.5 years of launch to 27% of ARR in 2023.

Github Copilot adoption was among the fastest new product lanches in terms of new products (~7% of total Github ARR). Though to be fair this could be seen more as a different SKU, to which this level of adoption is not too far away from NOW’s ~10% annual Pro Sku adoption increase

Snowflake has had the slowest new product launch among the vendors we have data for. For some of these companies, we don’t have the revenue numbers 2-3 years in as they don’t choose to disclose. BUT Databricks is one of the few has disclosed metrics for their SQL product (SNOW Datawarehouse competitor), and that product has seen penetration of 10%+ of ARR vs SNOW’s only 3% projected penetration of ARR of their Snowpark Product (Databricks competitor). Net net, this doesn’t look great for SNOW in terms of new product innovation/adoption, especially given the success of their own rival invading their own turf.

Monday.com (light blue dotted line) may not jump out to many, as it seems to be middle of the pack in terms of new product % penetration of after 1 year. However, the 3% of ARR penetration that MNDY has of their CRM Sales product launched in 2022, was done PRIMARILY via new customers, without much S&M $ investment, as they had not opened up the product to existing customers. The Sales CRM product is outpacing the core Monday.com adoption by a very wide margin. Monday has already rolled out a Dev product (Jira like) as well as an ITSM product that is yet to be launched later. Both the Sales CRM adoption + new product innovation could put MNDY on a path to be like HUBS in driving successful multi product adoption.

Source: Monday.com 2023 Investor Day

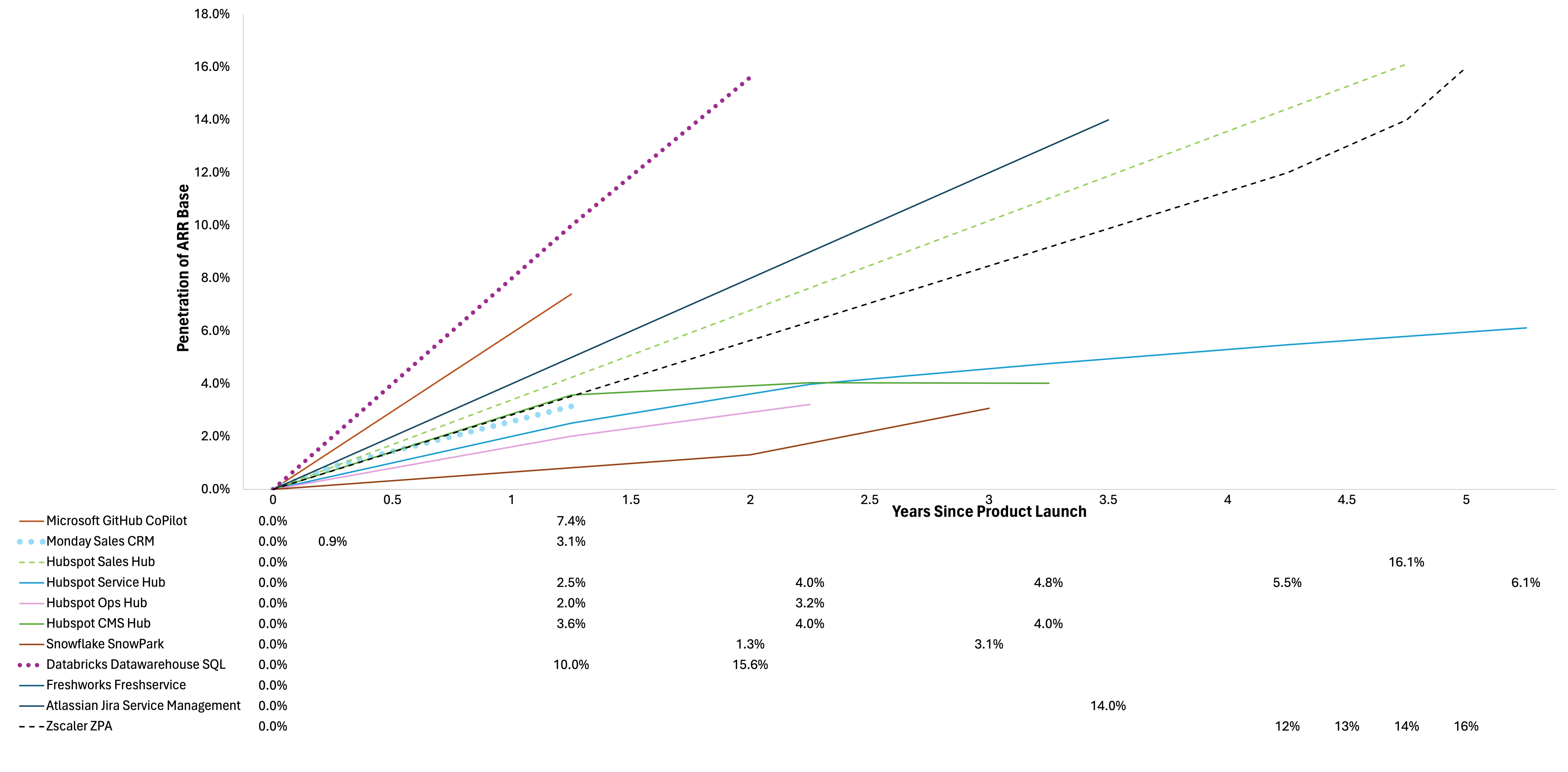

Bonus: A closer look narrowing the time period by 5 years post product launch.

**Sources:

Atlassian: Blog Post GA, 2024 Investor Day

Databricks: Bloomberg article, TechCrunch Article, Blog Post GA

Freshworks: S-1 Timeline, 2023 Investor Day

Hubspot: 2020-2024 Analyst Days

Monday.com: 2023 Investor Day, Sales CRM Blog Launch

Microsoft: The Information, Earnings Calls

Snowflake: 4Q24 Earnings Call, Blog Post GA

Zscaler: Various Earnings Calls