The Open Source Debate as a Technology Investor

The Open Source Debate as a Technology Investor

It’s Not Just in Software. Semis Also Has an Open Source Debate

Public Software investors have learned to be cautious with Open Source models, with very limited stories of success (MDB), those with mixed results (CFLT/Redhat), and those with “bad” results (ESTC/HCP). But the measure of “success” is often judged from the lense of “will this business be able to charge for a managed version” and “can it successfully scale monetization/margins”. In some cases admittedly there is the question of “will this technology be broadly adopted as the standard?” But even those that have become technology standards (Terraform), have been terrible businesses and ultimately bad public market investments (HCP/ESTC). What if I told you that Open Source is also a debate in the Semi’s World?

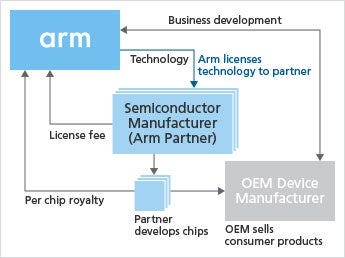

Meet ARM

ARM is one of the most important companies in the world and today boasts a market cap of +$100bn and an annual revenue base of $3bn. ARM provides an **ISA** or Instruction Set Architecture (more below) and does not manufacture chips but rather licenses IP of their instruction sets to chip makers.

Source: Softbank

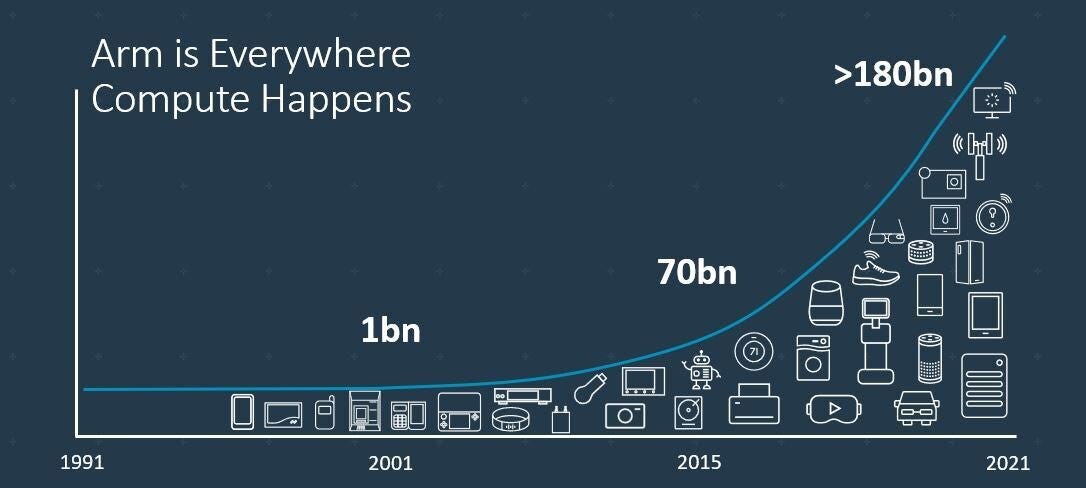

Today ARM has virtually 100% market share in mobile phones (it powers the iPhone and Apple devices today), a majority of IoT market, and has slowly started to dig into Intel’s lead on X86 on PCs (still very early on but approaching 10% market share). A crazy stat: 50% of all chips with processors are ARM-based.

Source: Softbank

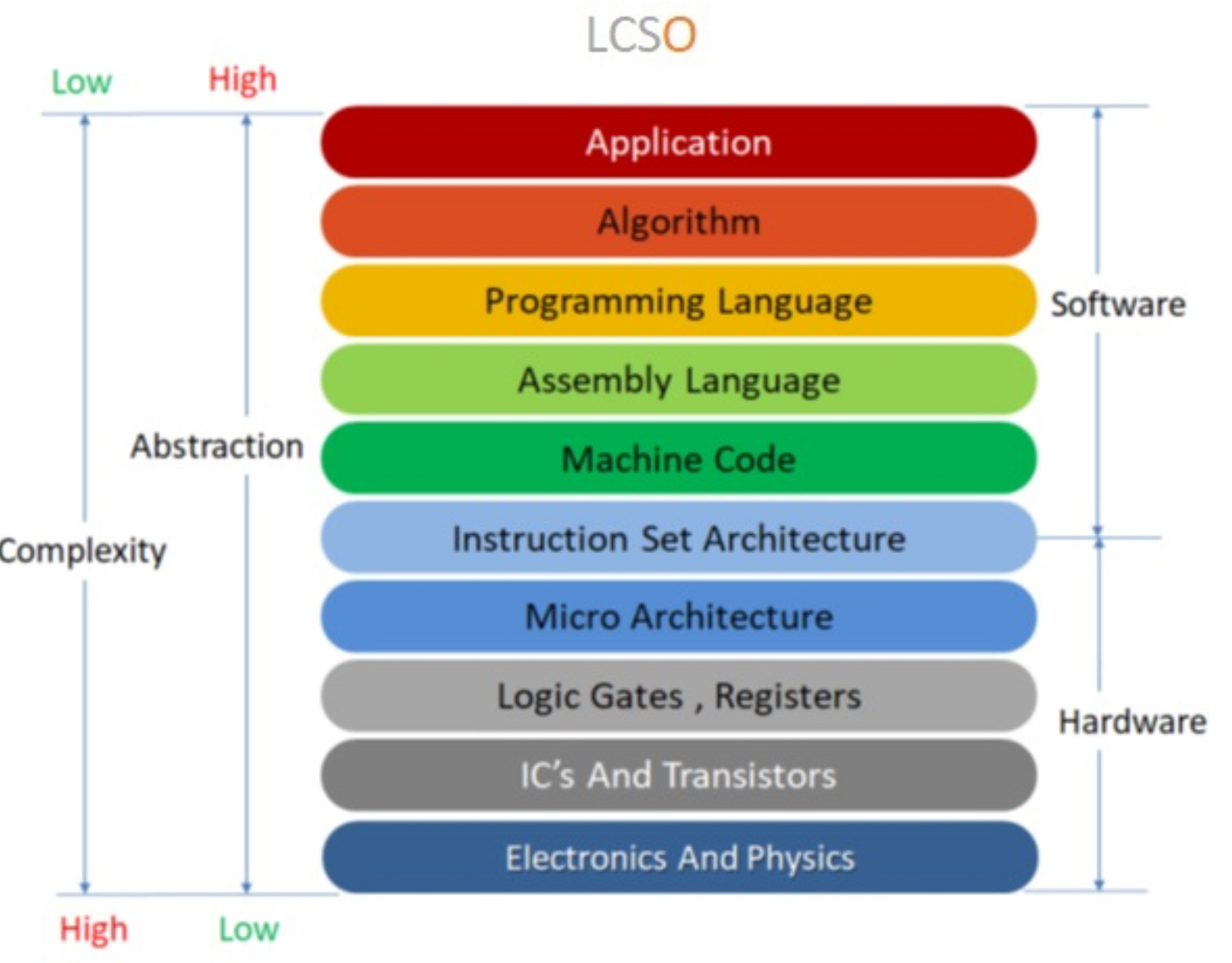

**Think of an ISA as a set of rules that helps connect software and hardware together, telling the hardware how it should act when it’s given a set of instructions. The more instructions or comments, the more complexity there is for the hardware to execute.**

Source: LCSO

ARM’s Open Source Threat

One of the risks to ARM’s business model LT (among others) is cited as RISC-V which at it’s core is similar to Linux or Apache in the Software world…a free Open Source Solution supported by a foundation. A quick search on Google indicates that, RISC-V International has over 4,000 members in 70 countries (though China is a big chunk of core users) including over 90 chip companies. The big kicker here is that among its members are the largest chip markers and thatInstruction Set Architecture from RISC-V can be used for commercial designs.

Instead of paying ARM for access to IP, those using RISC-V, even those that are not paying members, can get access to many of ARM’s most used designs. In theory this allows new entrants to rapidly enter the industry, potentially lowering the barrier to entry in newer markets. The only real credible large scale Semi vendor that is pushing RISC-V instead of ARM is QCOM (more on this later on).

Source: BAR & RISC-V

Quick Reflection on Software Investing in Open Source Models

Now a quick break and reflection on Software. Usually the founding members of an Open Source Project like ElasticSearch, eventually become commercial vendors (like ESTC) that charge customers and offer offering managed solutions that eliminate complexity of managing the technology. Although Open Source Software solutions are used by smaller companies, they are also used in production at scale at larger F500 companies who have the manpower to architect and maintain these solutions instead of paying a commercial vendor. The bigger “threat” for these Open Source Solutions are usually 1) losing relevance as new architectures gain adoption (Hadoop, potentially Pulsar/Sparq vs Kafka) & 2) monetization.

In the Software industry, higher adoption of the Open Source version of the software does not necessarily correlate with success of the commercial vendor, despite the commercial vendor often controlling what code/features get released into the free open source version (see HCP/ESTC as a primary example). In addition Open Source solutions in the software industry are usually not allowed to be used by another commercial vendor to develop competing products that can then be charged to customers. At the very least, license changes are made to restrict the latest version from being commercially available (see ESTC/MDB/HCP license changes). Software investors know very well the pain + joy of investing in Open Source Software companies.

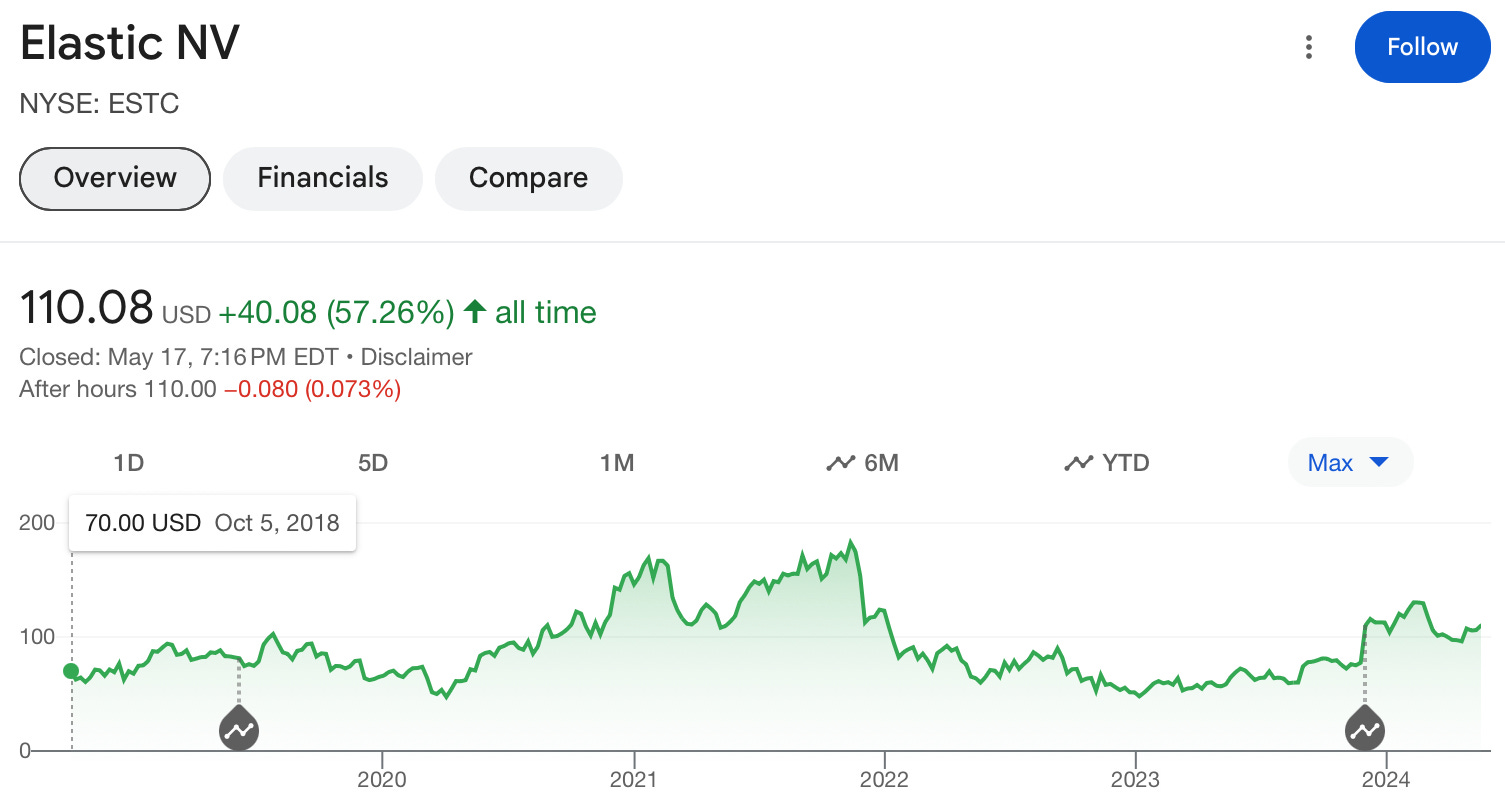

Source: Google Finance. Quick note that ESTC has had an <10% IRR since IPO in 2018 (this excludes the 1st day of trading where stock doubled, as hard to see how one could have built a full position on that day at the initial IPO price)

Potential Impact of RISC-V

In Semi’s, there is a completely different debate about the Open Source threat. In the case of ARM, the more obvious risk from RISC-V is from vendors like QCOM & STMicro that are encouraging RISC-V adoption. Those same vendors are members in the RISC-V foundation (including NVDA). In the case of wider adoption of RISC-V in chips vs using ARM’s IP, these chip makers would not have to pay ARM for access to their IP, which ARM usually charges through an initial license + royalty per device.

In fact QCOM has already started to ship chips with RISC-V standards instead of paying ARM (others like GOOG/INTC also now using). In 2019, QCOM started shipping the Snapdragon 865 with RISC-V instead of ARM. As of Sep of 2023, QCOM had shipped in excess of 650 million RISC-V cores (vs ARM has shipped over 230 billion chips to date). Other than QCOM I haven’t come across a serious Semi company trying to directly compete with ARM at scale through RISC-V. Here’s an interesting article on QCOM website on why they are pursuing this route.

Source: Qualcomm Website

Biggest Difference Between Software & Semis? Chips War.

At first glance it’s a big alarm bell for any real ARM investor, that in the market ARM dominates, large commercial vendors which control majority market share, could potentially start to disrupt a longstanding partner/leader. How much of this is just those vendors supporting the ecosystem or just a way for China to encourage more development of technology?

A second look at this situation and the divergence between this debate in Semis and Software becomes very clear. RISC-V seems much more of a threat to ARM’s China revenue (20% of revenue) than it is potentially taking away large ARM customers like Apple or Nvidia. In fact news reports (Reuters) points the US government becoming worried about Huawei and Alibaba’s adoption of RISC-V. Given how vested the US is in winning the Chips Wars, it does feel as if ARM has a bit of an advantage with the backing of the US Government vs an Open Source Software company with the backing of a VC firm.

Source: Reuters

Conclusion: Open Source is a Threat For Everyone.

There have been instances of Software investors believing that a Commercial vendor had enough differentiation on features/scalability, that Open Source was never a threat, only to discover that during tough times, free to paid conversion wilted and migration back to OSS occurred in a handful of instances (CFLT/HCP/ESTC all examples of this struggle in varying degrees). There have also been vendors in Software that have proven skeptics wrong as the competition with OSS was overblown (MDB).

ARM is coming from pretty much max market share in mobile & is gaining share in PC’s. So in theory given their position of dominance, they have more to lose than a small Software company that is trying to scale their business from $150m in ARR. That being said, if anything can be learned from looking at this topic, things are not as simple or as draconian as they can appear at first glance.

Nonetheless, both Software & Semis investors can rejoice in knowing that Open Source, is a somewhat of a threat to all.